.png)

The Energy White Paper 2012 (EWP2012), released by the Australian Government last week, seeks to map out a strategic policy framework for future energy supply. One of the major goals of EWP2012 is to provide a “clear vision” of how Australia should set about the long-term task of decarbonising our stationary electricity, liquid fuels and industrial sectors. So how well does it succeed?

The Energy White Paper 2012 (EWP2012), released by the Australian Government last week, seeks to map out a strategic policy framework for future energy supply. One of the major goals of EWP2012 is to provide a “clear vision” of how Australia should set about the long-term task of decarbonising our stationary electricity, liquid fuels and industrial sectors. So how well does it succeed?

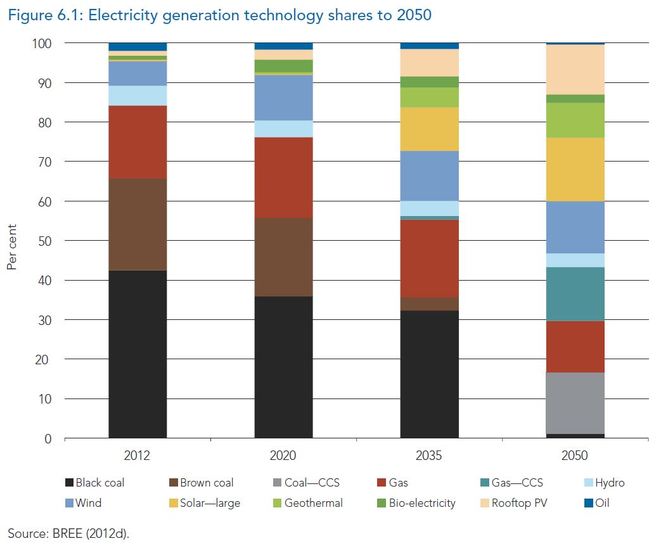

As an overview of the current status quo on domestic supply, distribution and exports of energy, it is a fine document. However, as a forward-looking, agenda-setting stimulus paper, it has weaknesses. The focus is strongly on how natural gas and unconventional fossil fuel markets might develop in the coming decades under various uncertainties, and the impact of these on national economic growth and trade. In terms of its projections of the expansion of currently poorly developed “alternative” (non-fossil) electricity – the biggest issue to address – let’s consider the medium-demand scenario (Fig. 6.1, pg 88):

This shows a gradual phase out of traditional coal (to be replaced by carbon-capture and storage [CCS] variants after about 2035) and a ramp-up of combined cycle gas (both CCS and non-CCS). Up to half of electricity is coming from wind, solar thermal, solar PV and engineered geothermal by 2050. The estimated cost is “more than $200 billion in new generation investment”.

This shows a gradual phase out of traditional coal (to be replaced by carbon-capture and storage [CCS] variants after about 2035) and a ramp-up of combined cycle gas (both CCS and non-CCS). Up to half of electricity is coming from wind, solar thermal, solar PV and engineered geothermal by 2050. The estimated cost is “more than $200 billion in new generation investment”.

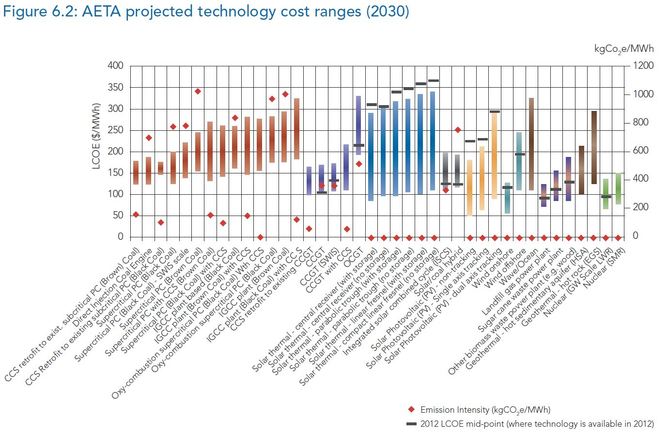

These projected finances are based on the levelised cost of electricity estimates provided in the recent AETA report, but do not adequately consider “value” of the electricity, as I explained here. Putting that to one side, the basic technology options, with current and projected 2030 prices, are shown in Fig. 6.2:

Nuclear power – generated by both large (“monolithic”) and small (“modular”) reactors – are an obvious low-cost, low-carbon (and baseload) standout here in Fig. 6.2. Yet nuclear power is invisible in the Fig. 6.1 projections.

Nuclear power – generated by both large (“monolithic”) and small (“modular”) reactors – are an obvious low-cost, low-carbon (and baseload) standout here in Fig. 6.2. Yet nuclear power is invisible in the Fig. 6.1 projections.

Why? This is explained in Box 6.3 on pg 98 of EWP2012. The argument made is that there is no “social consensus” on the technology (is there one for coal-seam gas?), nor an economic case (but that is relative to its direct competitor, black and brown coal, with no carbon price).

Filed under: Nuclear, Policy, Renewables, Scenarios | 2 Comments »